This is a post in view of the plenary on EU-China and Global Climate Policy at the Second Open Global Systems Science Conference, Monday 2pm: The report written by Yongsheng Zhang of the Development Research Center, Beijing, Carlo Jaeger of the Global Climate Forum, Berlin, and Emmanuel Guérin of IDDRI, Paris, will be available as hardcopy on the conference desk. We look forward to an exciting discussion at the conference. As usual, the debate can also continue here on the blog, both with comments to this post and additional posts.

Category Archives: Green Growth

Open Position: mathematical economist for green growth modeling

GCF, The Global Climate Forum, is looking for a mathematical economist to join our research team developing an innovative model of economic systems. The model shall be used for policy analysis in view of climate policy and green growth. Through the representation of multiple equilibria it will allow to identify win-win strategies for climate policy. The model will be applied to Germany, but its design shall allow for modifications to fit other countries and regions.

For more information on the position please download the job description.

For more information about the project go to German Green Growth Model.

Energy transition, climate change and financial crisis: zooming in and zooming out

The Global Climate Forum (Berlin) has started a series of workshops, which link new economic thinking to practical challenges in economic and environmental policy. The series aims at providing a productive setting to share current research efforts, to provide comments to and inspiration for each other’s work, and to engage in dialogues with relevant stakeholders. By doing so, we strive to establish a community of researchers who set standards for new economic thinking.

A good starting point for these kinds of dialogs was our first workshop, held on June 19th, 2012. More information can be found here.

A second workshop, held on December 11th 2012, discussed the topic “Energy sector transition – German madness or an opportunity for growth?”. This workshop included many inspiring presentations and discussions zooming into the electricity sector (at the German, Dutch, European and international level) and zooming out by assessing cross-sectoral effects as well as macroeconomic impacts. The vast knowledge of the matter among speakers and participants was very impressive and turned this into a promising endeavor.

To summarize the general ideas on green growth and some elements of the workshop discussions:

Climate crisis

Zooming out by looking at the latest climate negotiations in Copenhagen, Rio and Doha, the results are quite disappointing. No game changing decisions have been taken. Despite the strong evidence about climate change leading to large costs of climate adaptation in the distant (and not so distant) future, there is persistent inaction at a global scale.

There are even voices in Germany arguing that the currently proactive German and European approach increases incentives for other countries to free ride and is therefore not the best strategy. Germany should rather invest in adaptation instead of mitigation to increase its power in international climate negotiations. The cost of climate change adaptation would be much lower for Germany and therefore the urgent need for mitigation is not as high. But where will such a strategy take us? If framed like that, it is an example of a Prisoners Dilemma, and would lead to actively and consciously choosing for the inferior equilibrium. We should know better than that.

Financial crisis

On the other hand there is a seemingly never ending debt crisis in the Euro zone, fears of a fiscal cliff in the US, to name the most pressing financial challenges. These short-term and urgent matters are used as an excuse not to take any proactive decisions regarding long-term issues such as climate change. This is nicely picked up by a cartoon in the economist. However, if we reframe the problem, can a green investment strategy especially in southern European countries be a source of new and more sustainable growth and bring Europe back into balance? Can the trend of ever increasing youth unemployment rates and resulting social problems within countries and between the surplus and deficit countries be reversed?

Energy transition

Workshop focus: Zooming into the electricity sector and investigating the macroeconomic effects in Germany and elsewhere.

Germany has decided to phase out nuclear energy and to transform its energy sector into one based on renewable energy. The goal to raise the share of renewables in the energy market to 20% has been achieved. This largely happened due to the feed-in-tariff (guaranteeing a fixed price for renewable energy sold to the transmission system operators over 20 years) and without significant changes to the structure of the energy market. But striving towards an 80% share of renewables by 2050 will require massive changes in technology and infrastructure related to production, storage, grid and consumption, as well as associated transformations of governance structures and the market mechanisms themselves.

The transition is more complex than often thought. As an example, even if the costs for renewable energies reach grid parity (when the cost per kwh of solar power reaches the level of retail prices) this will not be enough to change the entire energy system. A household owning a photovoltaic panel will not use the power at the same time it is produced. Hence, this involves external costs in the form of storage costs, transport costs, additional capacity for flexible production or for demand side control. The supply and demand of electricity needs to be balanced, centralized or decentralized, and this will not come at zero cost.

Other countries are watching Germany with a skeptical eye. But why is nobody talking about the positive external effects of such a strategy? It will reduce CO2 emissions and in terms of climate change mitigation everyone will benefit from it.

Instead, the negative effects on neighboring countries are emphasized a lot lately, for example by the French Centre d’Analyse Strategique saying that the Energiewende comes at a high cost for the consumer and is endangering the equilibrium of the European energy system. However, this would assume that the system is in some kind of equilibrium, which is questionable.

The European energy system as a whole is characterized by opportunistic national decisions, not aimed at finding efficient solutions for the European system as a whole. Hence, all countries need to concentrate on how we can better cooperate on a European level with respect to energy production and consumption.

Can Germany show that the energy transition will become an economic opportunity by 2020?

Can the energy transition be regarded as a potential source of economic growth, where innovation and technological advances increase energy efficiency and general productivity? And more importantly, can it help overcome the reluctance in international climate negotiations on the one hand and serve as a viable and sustainable exit strategy from the negative feedback loop of austerity policies, low investment, low employment and low growth in the Euro zone, on the other?

How can these seemingly unconnected discussions on climate change, the financial crisis and the energy transition be combined? Success of the global climate negotiations are a necessary, but not sufficient condition for a more sustainable future. The discussions need to become broader and include the interrelatedness of the problems. This requires new ideas and new concepts. Can green growth be such a new concept?

Green Growth

Zooming out again, there is much talk about green growth, no growth, de-growth and so forth. Which opportunities lie within a green growth strategy?

The general goal is to reach a superior equilibrium resulting in win-win situations in a social, environmental and economic dimension. We can reach this with a national (or international) commitment combined with proactive policies triggering a (public and private) green investment surge into renewable energies, renewing the built environment and energy efficiency measures in industry and transport at a large scale. A transition to a new growth path entails more than an energy sector transition alone.

Therefore, the German energy transition needs to be put into perspective. It will not succeed by 2020 if carried out without additional measures. Especially important are the effects on other sectors and the resulting impacts on the economy as a whole.

As an example, the increasing price for electricity associated with the energy transition is subject to much criticism within Germany and abroad. But is this the whole story? If the price of one unit of electricity (kWh) rises but if we can use this much more efficiently then the overall energy bill doesn’t necessarily have to rise. Additionally, if a country were to pursue a green growth strategy and largely invest in a transformation process, including renewable energy and energy efficiency in buildings, industry and transportation, this would increase the national income and reduce energy usage and CO2 emissions at the same time. A higher national income will translate into increased turnover of firms and wages of workers, and can more than compensate for increased energy bills.

Lack of attention to this broader picture is a barrier currently suspending any movement towards pursuing a green growth strategy. We cannot zoom into a specific sector and neglect the interactions on cross-sector and on macroeconomic level.

New Economic Thinking

Generally speaking we need to look at the problems at hand in a more holistic way.

There is an urgent need for a professional dialogue about the tools that economists can develop to help design and assess suitable policies. What is needed is more than the standard neoclassical approach. Assessments need to go beyond single equilibrium models and include the possibility of multiple equilibria. Furthermore, we need to investigate the relevant agents, their interactions and the networks they engage in, the set of choices they have and the governance arrangements hindering or promoting a transition. This can be done with agent based models for example.

Furthermore, there is a need to discuss these models with policy makers, to whom they should provide more insight into the dynamics of the problem at hand.

Further information

For a summary of the workshop as well as the workshop presentations click here.

For further interesting contributions, also read Klaus Hasselmann’s latest post.

Climate Policy – Reference

An agent-based model dealing with climate policy which combines social systems operating on multiple levels (local, national, and international)

http://www.sciencedirect.com/science/article/pii/S1364815212002332

Green Growth in Global Systems Science

ECB President Mario Draghi, on September 6th, 2012, stated that

the assessment of the Governing Council is that we are in a situation now where you have large parts of the euro area in what we call a “bad equilibrium“, namely an equilibrium where you may have self-fulfilling expectations that feed upon themselves and generate very adverse scenarios. [see here]

At the same time, the current fossil-fuel-based economy, with its CO2 emissions, constitutes a “bad equilibrium” for the climate system. Green growth as a strategy to move from a bad equilibrium to a good one in these two dimensions seems a worthy research topic for global systems science. The Eurozone crisis and sustainability are largely discussed in disjoint debates. Global systems science could combine these two current challenges in order to identify cross-benefits between policies targeted at either one of them.

Germany’s “Energiewende” – a transformation towards an energy-efficient and green economy – could be an element of a strategy to move to a better equilibrium. Unfortunately, the recent public debate in Germany seems to be missing this point. Started off by the announcement that electricity prices will rise, due to a rising feed-in-tariff levy for renewable energy, the debate centers around these costs, and for the most part overlooks benefits that a consequently pursued green growth strategy would entail.

German Green Growth Model

We – the Lagom research group at the Global Climate Forum – are working on a model to study green growth opportunities, with a focus on Germany. The model shall be made available in a modular open-source framework, so that it can be combined with existing models providing more detail on particular sectors. By explicitly representing the possibility of multiple equilibria and corresponding growth paths for the economy in general, and the strongest European economy in particular, our research contributes important building blocks to the emerging Global Systems Science.

More detailed information on the project can be found here. The model development is based on a manifold dialogue with potential model users, experts of existing models, new economic thinkers and the general public. To extend this dialogue into the virtual world, we kindly invite comments, as well as a broader discussion of the arguments merely sketched above, on this blog.

The Euro-Crisis: North, South – and the East?

The Euro-Crisis: North, South – and the East?

Alan Greenspan is not the only one to believe that “Europe’s crisis is all about the north-south split” (Financial Times[1], Oct. 9, 2011) This idea has become particularly influential through widespread claims that the way to overcome the Euro-crisis is for Greece and other Mediterranean countries to follow the shining example of Latvia and the other Baltic countries. Such claims have been endorsed by highly influential figures like Christine Lagarde, the IMF head[2] and Jörg Asmussen, Germany’s representative on the Executive Board of the European Central Bank[3].

With regard to the financial crisis, the number one success story among European countries is not Latvia, but Poland (Figure 1). In fact, the people of Latvia – especially those of Russian origin – have experienced some of the hardest pain seen across all over Europe, with little reward except for the praise they sometimes get for achieving outcomes vastly outperformed by Poland. Against that background, it is useful to look more closely in the experience of Eastern European countries. Perhaps there is something to be learned here.

Figure 1, Changes – Governmental purchases vs. real GDP

Source; http://krugman.blogs.nytimes.com/2012/02/18/austerity-and-growth

At least three features of the Polish experience deserve particular attention:

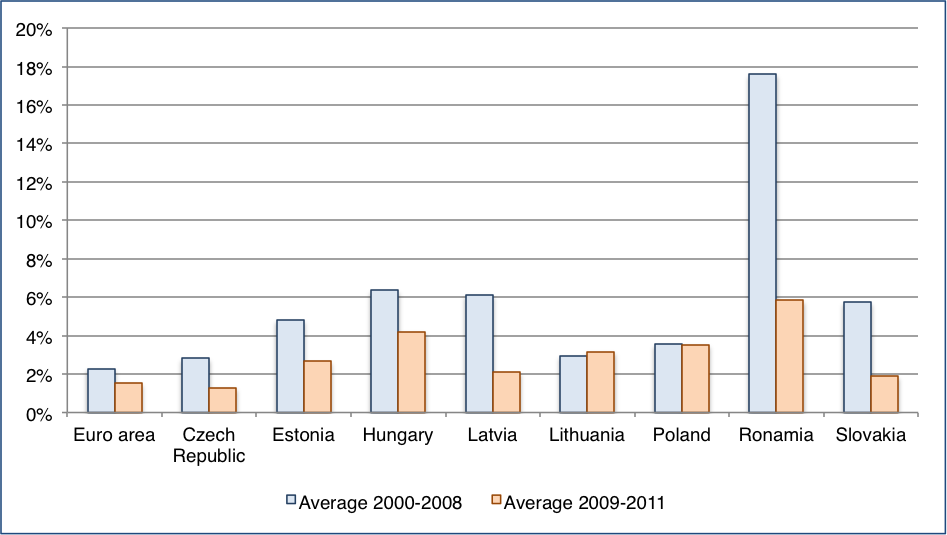

First: While the European Central Bank sticks to its pre-crisis definition of price stability as somewhat less than 2% of inflation (a perfectly arbitrary threshold), Polish inflation was about 50% higher, i.e. around 3%. Figure 2 depicts this fact: while most countries – as well the whole Eurozone – had a significant reduction of inflation since the crisis, Poland stayed at a moderate level of 3-4% over the last decade.

{kind=link}

Figure 2, Average inflation in Euro area and NMS states 2000-2011, Source Eurostat

At the same time, while the Eurozone had a decrease of money supply by 3% in 2009, Poland expanded the Zloty supply by 10% and followed an expansive money policy also in 2010. Latvia, Lithuania and at some extent also Bulgaria, Estonia and Romania decreased their money supply when the crisis started (Figure 3).

, 2005-2011")

Figure 3, Percentage change in money aggregates (M1, M2, M3), 2005-2011, Source, Eurostat

Second: While those Eurozone countries where the financial crisis led to a sudden stop of capital inflows had no national currency to devaluate, Poland absorbed part of the financial shock by a temporary devaluation of the Zloty (-30% from October 2008 to March 2009 in relation to the Euro) which decreased labor costs and enhanced the internal and external competitive position of the Polish economy. This was enabled by the Polish floating exchange rate. In comparison, Latvia, Lithuania and Estonia have euro peg currencies.

Third: While Eurozone countries in distress were put under massive pressure to reduce their government’s expenditures, Poland did in fact increase government expenditure in 2009 and 2010 (see Figure 4 and Figure 5).

Figure 4, Percentage changes in governmental expenditures, 2008-2011, Source, Eurostat

Figure 5, Percentage changes in governmental consumption, 2008-2010, Source, Eurostat

Since 2005, Poland kept increasing gross investment while Latvia kept decreasing it after the crisis (Figure 6).

Figure 6, Governmental expenditures for Gross Investments in % of GDP, Source, Eurostat

Figure 7, New governmental indebtedness in % of GDP, Source, Eurostat

While the EU27 and the Eurozone have a deficit of more than 80% of annual GDP, the deficit of the New Member States (except Hungary) is significant less (Figure 8).

Between 2000 and 2007 all EU27 countries (with the exception of Hungary and Poland) reduced their deficit between 1.4% (Estonia) and 55% (Bulgaria). Over the same period, Hungary increased its deficit starting by 11% from a relatively high level in 2000 and Poland by 8.2%.

As a result of the crisis, the growth of deficits between 2008 and 2011 was significant for Latvia (+115%), Lithuania (+148%), Romania (+149%) and Slovenia (+117%).

Comparatively, the Polish situation was less dramatic: the increase of the deficit between 2000 and 2007 was of 8.2% and since 2008 of 20%.

Figure 8, Governmental deficit, % of GDP (bar) and changes 2008-2011 (dot) in %, Source, Eurostat

Poland and Czech Republic were the only two countries, which increased their GDP in 2008. Comparatively, the Baltic countries had a significant reduction in their growth rates: Estonia from 20% to 1%, Latvia from 32% to 9% and Lithuania from 19% to 13% (Figure 9). After a decline in 2009 of 14% Poland was the only country, which recover in 2010 completely, being back to a pre-crisis level.

Figure 9, Average annual GDP growth, 2000-2008 and 2008-2011, Source, Eurostat

While this post attempts to bring into light some of the facts characterizing the economic situation of Poland and of the Baltic countries, we are obviously aware that all of the above constitutes only part of the story. Indeed, further socio-economic circumstances, institutional structures and cultural determinants have their influence on the development of the East Europe and it is not obvious that one or the other political decision brought success in Poland. However, it is important not to overlook Poland when looking for shiny examples of how countries handled and still handle the crisis.